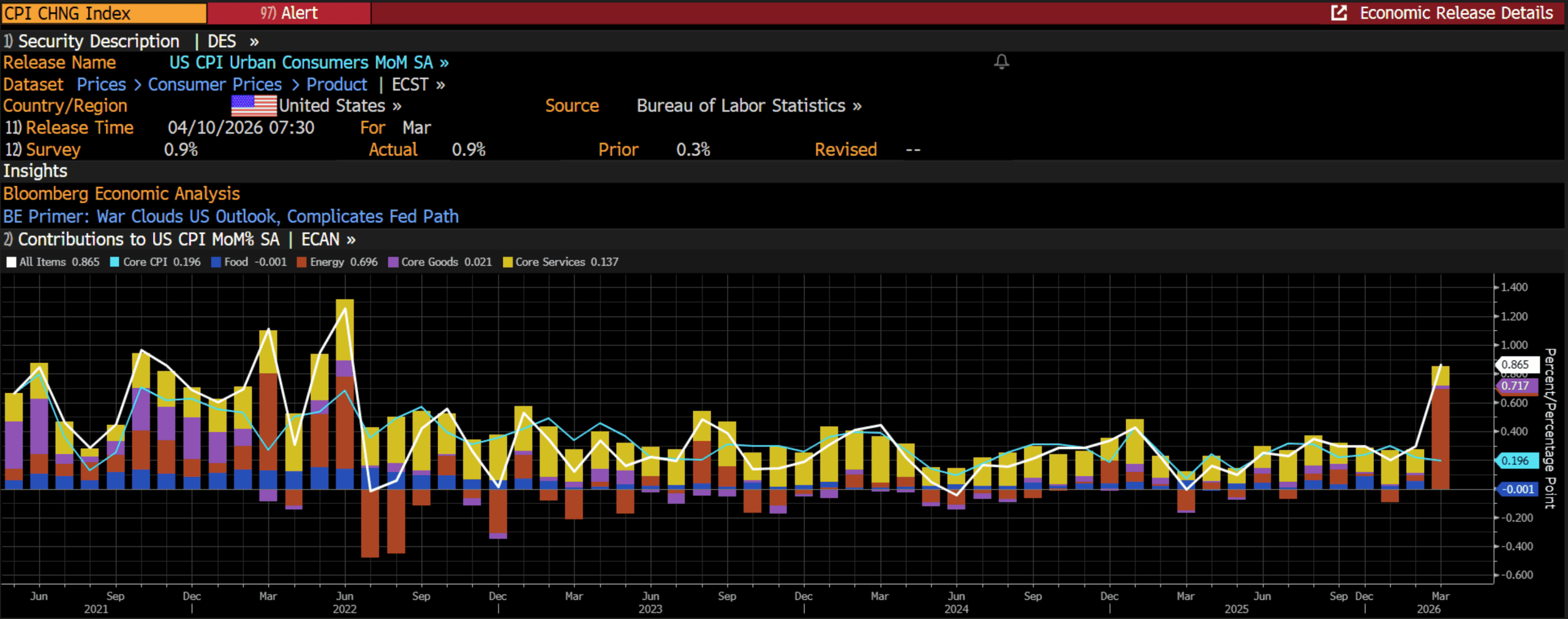

As expected, inflation surged in March, marking the first clear transmission of geopolitical risk into U.S. consumer prices. This morning’s release of the Consumer Price Index (CPI) showed prices jumped 0.9% last month, the largest monthly increase in nearly four years, when prices soared in response to the Russia-Ukraine war. The move was driven primarily by the surge in oil prices following the escalation of conflict with Iran, alongside the continued pass-through of tariffs into consumer goods.

On a year-over-year basis, headline CPI accelerated to 3.3%, reversing the prior cooling trend but landing squarely in line with expectations. The primary catalyst behind the move was unquestionably energy. Global crude prices have risen more than 30% since the onset of the conflict, pushing gasoline prices above $4 per gallon nationally for the first time in over three years. As is typically the case, this translated quickly into headline inflation.

Beneath the surface, inflation dynamics were more measured. Core CPI, which strips out volatile food and energy prices, increased 0.2% month-over-month, unchanged from February. The year-over-year pace edged up modestly to 2.6%. While this stability is somewhat reassuring, it likely understates the forward trajectory.

The surge in energy prices may represent just the first phase of the inflation impact. March data incorporated the immediate effect of higher oil prices, but the broader economic effects, particularly through diesel and transportation costs, are still working their way through the system.

Energy shocks rarely remain isolated. As higher fuel costs ripple through the economy, several second-order effects are expected to materialize. Rising airfares, driven by higher jet fuel costs are expected as are increased transportation and distribution expenses tied to diesel. Furthermore, we could see upward pressure on goods prices, including fertilizers, plastics, and other energy-intensive inputs.

Sustained price pressures, particularly in essentials like gasoline, may have third-order effects on the economy as well if they begin to erode household purchasing power and weigh on consumption. Ultimately, the path forward may hinge on the consumer response. If households absorb higher gasoline prices without materially altering spending behavior, businesses may retain pricing power, allowing inflation pressures to broaden. However, if consumers begin to pull back it could limit the ability of firms to pass through rising costs and weaken labor market dynamics as well.

All of this brings a tremendous degree of uncertainty into the economic outlook and a more challenging backdrop for Fed policy. The Fed has maintained a heavily data-driven stance and will be closely watching how these effects begin to play out in the data. To that end, we have a full docket of economic news to look forward to next week but for now, enjoy the weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrea F. Pringle

Senior Vice President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.