Markets this week contended with more headlines of increasing inflation, elevated oil prices, and intensifying geopolitical tensions. At the center of the week’s news was the latest from the Federal Reserve, which held its benchmark policy rate steady at 3.5%–3.75%, in line with expectations. However, the decision carried a notably hawkish undertone. In what was the final meeting chaired by Jerome Powell, the FOMC delivered its most divided outcome since 1992, with four dissenting votes. Notably, three dissenters pushed back against the Committee’s perceived easing bias over their discomfort with the notion of signaling future rate cuts, while one member dissented in favor of an outright cut.

The internal division underscores a growing tension within the Fed as inflation risks remain elevated. Markets responded accordingly. The few expectations for policy easing in 2026 were completely erased, and rate futures briefly priced in the probability of additional tightening. The shift reflects mounting concern that inflationary pressures, particularly those tied to energy, could prove more persistent than previously anticipated. Oil prices, which are the leading upside risk to inflation, hit a new four-year high on Thursday over concerns that the Iran war could worsen with the U.S. reportedly considering military action to break the negotiation deadlock.

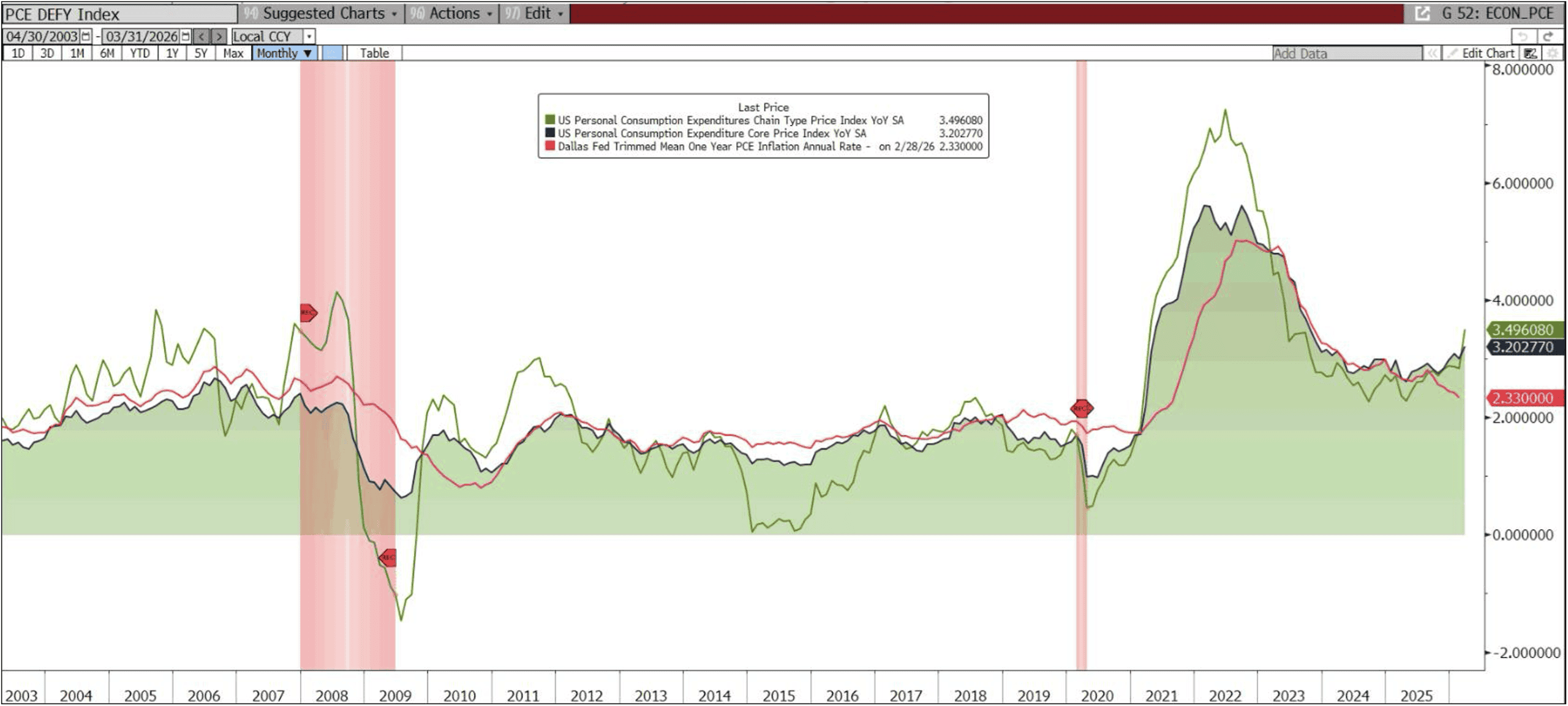

Incoming economic data did little to assuage those inflation fears. The Fed’s preferred consumer price gauge, core PCE, rose 0.3% month-over-month in March, pushing the annual rate to 3.2%, its highest level since late 2023. The broader headline measure showed even firmer readings, with headline PCE running at 3.5% year-over-year (+0.7% MoM). While the data came in line with expectations, it reinforced the narrative that inflation remains above target and is no longer on a clearly declining path.

Thursday’s GDP data showed the economy continues to expand, but at a moderate pace. First-quarter GDP grew at a 2.0% annualized rate, rebounding from a sluggish 0.5% pace in the prior quarter but falling slightly short of expectations (+2.2%). The composition of growth was somewhat encouraging with consumer spending, the backbone of the U.S. economy, rising 1.6% driven primarily by services demand. However, the overall growth profile suggests an economy that is not accelerating meaningfully, even amid structural tailwinds such as increased investment in AI and the resumption of normal government activity following last quarter’s shutdown.

Overlaying the macro and policy developments was a notable escalation in geopolitical and energy market uncertainty. The Organization of the Petroleum Exporting Countries (OPEC) faced a significant disruption as the United Arab Emirates announced its decision to exit the cartel. The move highlights deepening fractures within the group and raises questions about OPEC’s ability to coordinate supply effectively. At a time when global energy markets are already strained by geopolitical conflict, the development adds another layer of uncertainty to the inflation outlook.

Next week is the all-important “jobs week” with a flurry of data due out on the state of labor market. Have a great weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrea F. Pringle

Senior Vice President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.