The holiday-shortened week is ending with some optimism around an apparent U.S.-Iran ceasefire extension. The circumstances remain fragile given the many advances that have failed to materialize in previous negotiations but there are signs of progress. On Thursday, US officials reported the two countries had agreed to a deal framework that would extend the ceasefire for 60 days and initiate a dialogue on the future of Iran's nuclear program. The deal reportedly could allow unrestricted passage through the Strait of Hormuz and give Iran 30 days to remove mines from the passageway. The U.S. would also lift its blockade on the Strait and issue sanction waivers allowing Iran to resume selling oil. However, the deal has yet to receive official approval from President Trump or Iranian leadership. Markets are taking the news positively heading into the weekend with equities pushing higher and crude prices moving lower.

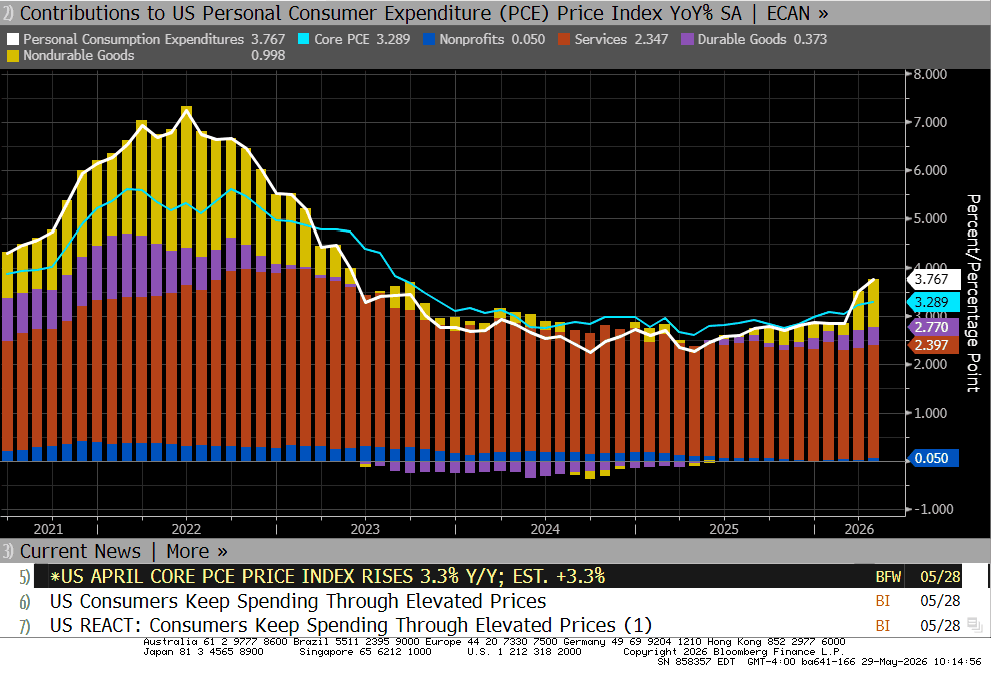

The rest of the week’s economic data was less positive. On Thursday, Q1 real GDP was revised down to 1.6% annualized from the initial 2.0% estimate with AI investment the apparent main driver of growth. April’s Personal Consumption Expenditures (PCE) index rose 0.4% MoM (vs 0.5% consensus) and 3.8% YoY. While inflation is clearly ticking up, the core measure, which strips out food and energy, was less pronounced. Core PCE came in at 0.2% MoM (vs 0.3% consensus), which marked the lightest reading since November. Core PCE was up 3.3% for the year, in line with expectations.

Thursday’s personal income and spending data for the month of April also painted a somewhat worrying picture of the American consumer. Income growth came in flat on the month, a significant miss from the 0.4% consensus estimate. However, spending still managed to meet expectations, rising 0.5% over the month. With income flat, Americans are clearly relying on savings to fuel that spending increase. The savings rate has drawn down to a near four-year low of 2.6%, a full three percentage points below where it stood just four months ago. Spending growth appears increasingly detached from income growth, propped up by wealth effects among higher-income households and a surge in credit card usage further down the income ladder. Unpaid credit card balances are now at a record $1.3 trillion and 90-day delinquency rates are above 13% for the first time in 15 years.

Consumer confidence is clearly reflecting that strain. The Conference Board’s Consumer Confidence index edged down to 93.1 from a revised 93.8 in April. The present situation reading fell to 121.1 from 124.4, approaching its five-year low. The "jobs are plentiful" component of the survey dropped to 25.5%, the lowest since early 2021. Consumers' 12-month inflation expectations held at 6.2% YoY, and 62.2% of respondents expect higher interest rates, near the highest since August 2023.

The U.S.-Iran war and resulting closure of the Strait of Hormuz is the dominant backdrop for the economic outlook, but we will also get fresh readings on the state of the labor market next week. Friday's May non-farm payrolls are expected to show jobs growth slowing to 93k and the unemployment rate holding steady 4.3%. Have a great weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrea F. Pringle

Senior Vice President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.