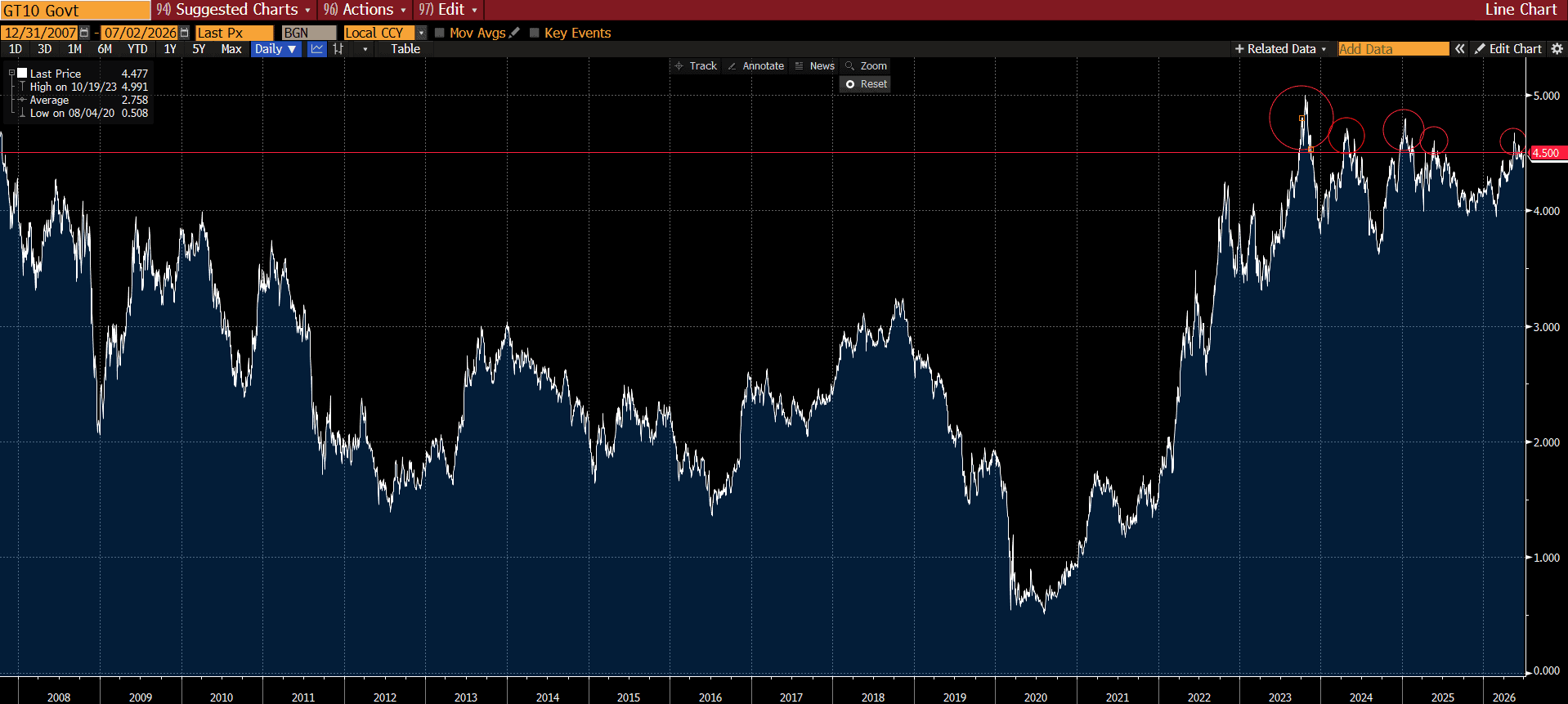

It seems like you blink once after the New Year and it's already July. Blink again and our great country is turning 250 years old (although she doesn't look a day over 249). And while we're on the topic of milestones, it seems relevant to mention the 10yr Treasury, which peaked above 4.50% last week and is currently trading at 4.48% as of the time of this writing. Breaching the 4.5% yield threshold has been a very rare occurrence, happening in only 5 short trading periods, going all the way back to the end of 2007. Put another way, if you’re a portfolio manager coming up on 20yrs of experience, today’s yields are higher than they’ve been for approximately 97% of your career.

This morning's employment report helped to nudge those yields a bit lower as the economy added just 57k jobs in June (est = 113k), and revisions took another 74k off the prior two months. That pulls the three-month average down to 111k from the 188k we reported last month. The gains were again concentrated in health care (+47k) and private education (+22k), while leisure & hospitality (-61k), retail trade (-8k), and mining (-4k) saw the largest declines.

The separate household survey told an even weaker story, showing a loss of 507k jobs, the fifth monthly decline in the past six. Yet despite the soft payroll print and the drop in household employment, the unemployment rate unexpectedly fell to 4.2% (est = 4.3%). This change is driven more by attrition than it is by strength in the labor market as 832,000 people left the labor force, and the participation rate, the share of the working-age population either employed or looking for work, plunged to 61.5% (est = 61.8%). That rate is now down a full percentage point since November, with the labor force shrinking by 2.2mm even as the population grew by 533k. Outside of the pandemic, that is the steepest participation decline over any comparable stretch on record. That doesn’t quite point to a healthy labor market, and this report has the potential to meaningfully reshape the discussion at the next FOMC meeting, particularly if the coming CPI shows inflation moderating on the back of falling oil and gasoline prices.

The rest of the week's data pointed in the same cooling direction. ISM manufacturing eased to 53.3 (est = 53.9), still in expansion but a step slower, and consumer confidence slipped to 91.2 (est = 94.4). More encouraging for the inflation outlook, the ISM prices-paid index, the survey's gauge of input costs, fell sharply to 73.0 from 82.1, a sign that cost pressures are cooling alongside the drop in energy prices. Initial jobless claims held near 215k, announced layoffs are running modestly below year-ago levels, and job openings were still elevated at 7.6mm in May compared to the last 2 years, so the weakness appears to be concentrated in participation and the household survey rather than in outright layoffs.

Fed Funds Futures still lean toward the Fed's next move being a hike rather than a cut. The market is pricing only about 18% chance of a hike at the July 29 meeting and an implied path that peaks near 4% in the first half of 2027. The swing factor from here will likely be the June CPI report on July 14, which will capture a 28% drop in oil prices and a 16% decline at the pump. A soft reading there would give the doves real ammunition.

Looking ahead, next week is lighter on marquee data but we do get a look at the June FOMC meeting minutes on Wednesday which will detail Chairman Warsh’s first meeting. This will provide the market with the first detailed look at how the committee reasoned through dropping its easing bias.

Hope everyone has a great (and safe) holiday weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dillon Wiedemann

Senior Vice President of FSG

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.