Geopolitical risk returned to the forefront this week as the U.S.-Iran ceasefire collapsed. Attacks on commercial tankers in the Strait of Hormuz prompted military exchanges between the two nations and the reimposition of a U.S. naval blockade of the Strait. Despite the severity of the escalation, energy markets responded with relative restraint. Brent crude traded near $85 a barrel heading into Friday — up more than 12% on the week, but still well below the wartime high of approximately $118. The muted reaction suggests markets are pricing in a near-term de-escalation, though the path to normalization for energy markets is by no means straightforward.

Global oil inventories, which were flush when hostilities first broke out in February, have since drawn down considerably. Meanwhile, alternative transit routes are increasingly at risk, as Iran has called on Yemen's Houthis to close the Red Sea oil route if the U.S. strikes Iranian power infrastructure. With both primary and secondary supply routes potentially in play, the current calm in energy markets may prove short-lived.

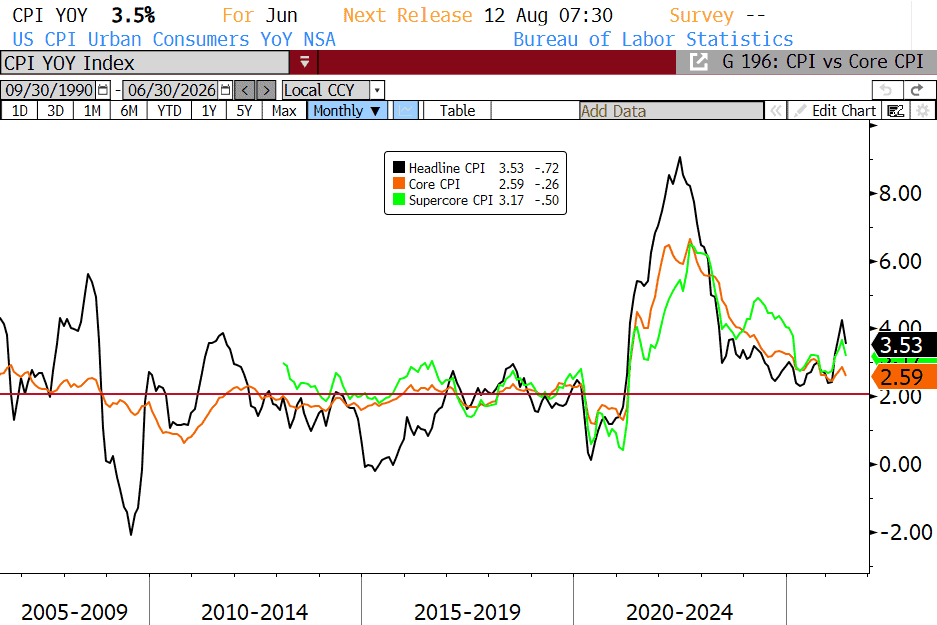

The notable bright spot for the week was Tuesday's Consumer Price Index (CPI) report for the month of June. Headline CPI rose 3.5% year-over-year, below the 3.8% consensus estimate, while core CPI — excluding food and energy — decelerated to 2.6% from 2.9% the prior month. The monthly reading registered its first decline in six years with the index falling 0.4% since May. The pullback in CPI mostly reflected a decline in energy costs, particularly a 9.7% drop in gasoline prices, a development unlikely to be repeated in July. The national average for gasoline has already risen to $3.86 a gallon, with further increases expected as oil prices respond to renewed hostilities.

Federal Reserve Chair Kevin Warsh offered little in the way of forward guidance during his congressional testimony on Monday, reaffirming the Fed's commitment to returning inflation to its 2% target while stopping well short of signaling any imminent policy shift. Rate hike expectations remain intact for later in the year. The renewed conflict in the Middle East has preserved the possibility of additional tightening should energy prices reignite broader inflationary pressures.

The economic calendar is light next week, with earnings season providing the primary market catalyst. The trajectory of oil prices and the evolving situation in the Gulf, however, are likely to remain the dominant variables shaping market sentiment as we move through the second half of July.

Have a great weekend!

Source: Bloomberg Finance L.P.

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrea F. Pringle

Senior Vice President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.