The final week of August left markets whipsawed between dovish signals from the Federal Reserve and rising political risk around its independence. Fed Governor Christopher Waller, widely reported to be one of President Trump’s leading picks to replace Chairman Powell when his term expires next year, all but confirmed that rate cuts are coming in a speech to the Economic Club of Miami this week. Waller said he would back a 25 basis point cut in September, with more easing expected over the next 3–6 months.

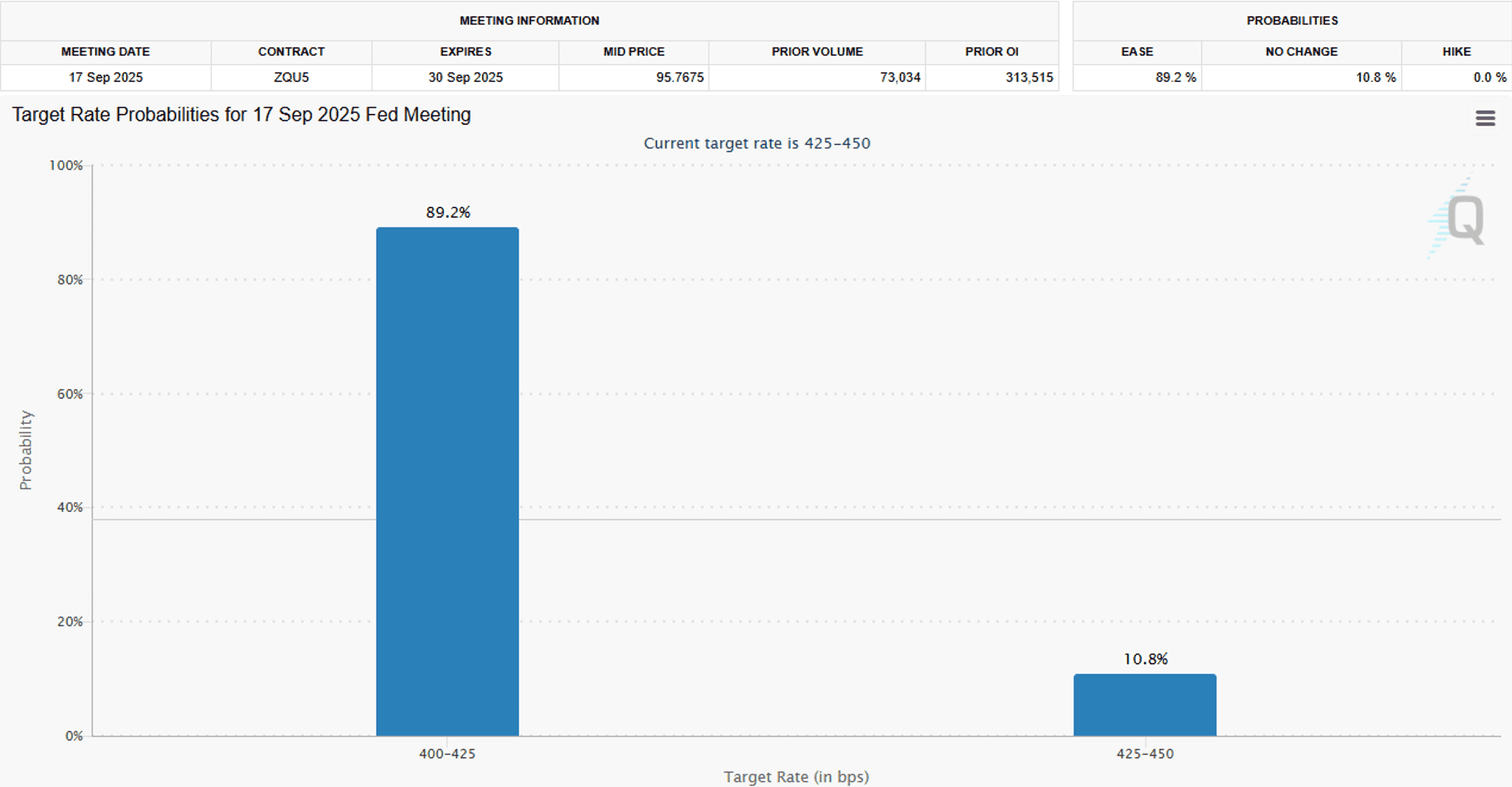

He also argued that inflation is now near target and the bigger risk is a rapid labor-market deterioration, noting job growth has slowed to just 35,000 per month since May. Waller told the audience that the Fed should not “wait until deterioration is under way” before acting. Chairman Powell struck a more cautious tone in his Jackson Hole address last Friday but also acknowledged that downside risks are rising. The futures market has clearly bought into this dovish shift in the Fed’s tone and is currently pricing in a near 90% probability of a September rate cut with a gradual easing path continuing into year end.

One of the biggest wildcards in the path to lower rates is the potential for President Trump to reshape the central bank, a possibility that has already resulted in long term yields moving higher this week. The President’s move to fire Fed Governor Lisa Cook on Monday over allegations of improper mortgage borrowing could give him a chance to install a majority of his picks on the Board by next year. Cook is currently challenging the legality of this move in court, but this unprecedented square-off between the White House and the Fed has sparked fresh concerns about central bank independence. In response, the 2-to-30-year part of the yield curve moved to its steepest since January 2022 as markets fear a more politically aligned Fed could tilt decisively dovish, weakening the dollar and further steepening the yield curve.

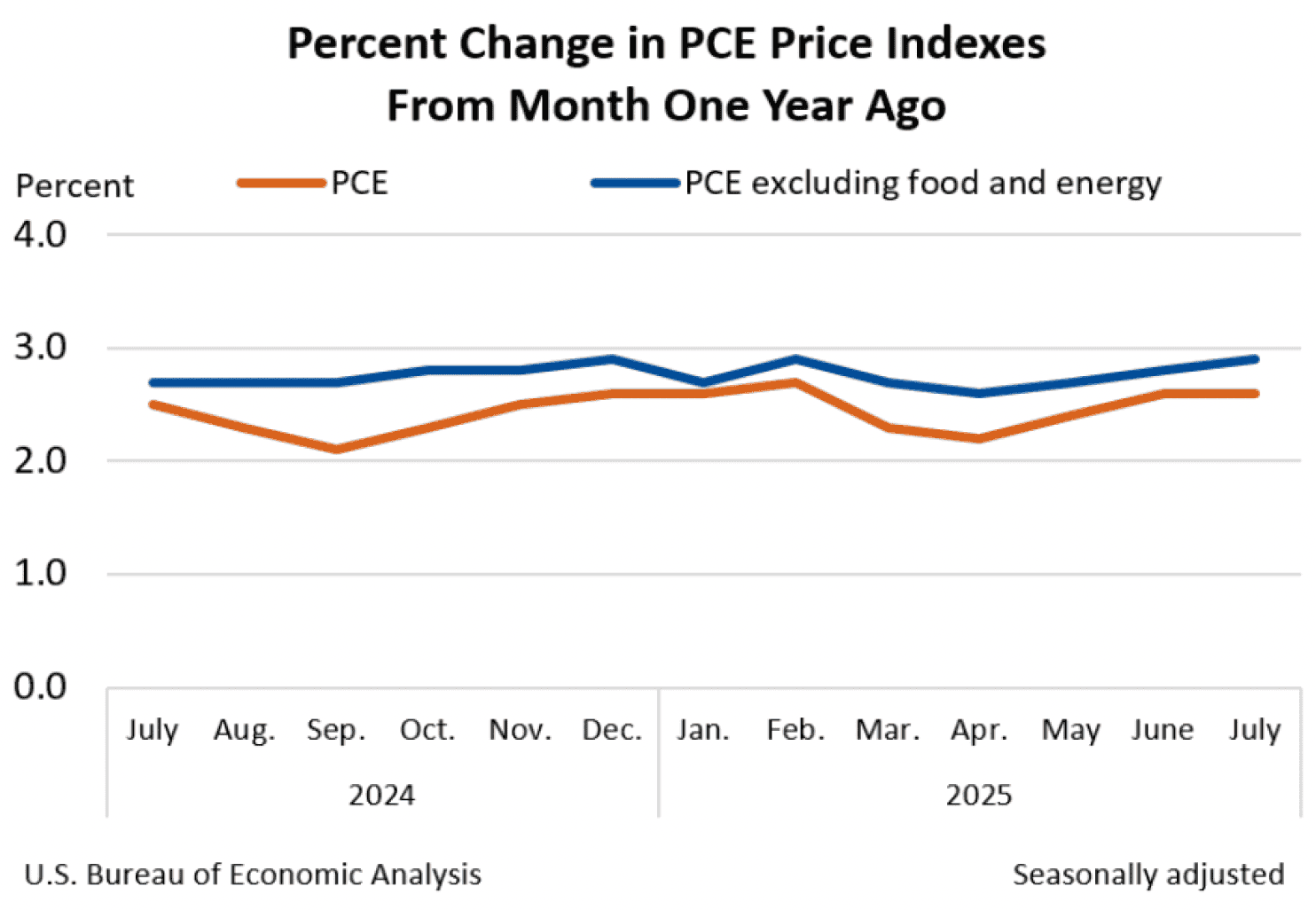

The inflation outlook remains another complicating factor as well. Waller noted in his address this week that while new tariffs risk adding near-term price pressures, these should peak by early 2026. For now, inflation expectations remain well anchored, giving the Fed breathing room to ease next month. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) index, was also released this morning and showed little sign of resurging inflation. PCE rose 2.6% in July on an annualized basis, in line with market expectations. Core PCE, which strips out food and energy prices, showed an increase to 2.9%, a slight acceleration from June.

Incoming data remains pivotal and next week’s August jobs report looms especially large. A weak print could cement the case for not just one cut, but a string of them into year-end. Hope everyone has a very happy long weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrea F. Pringle

Senior Vice President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.