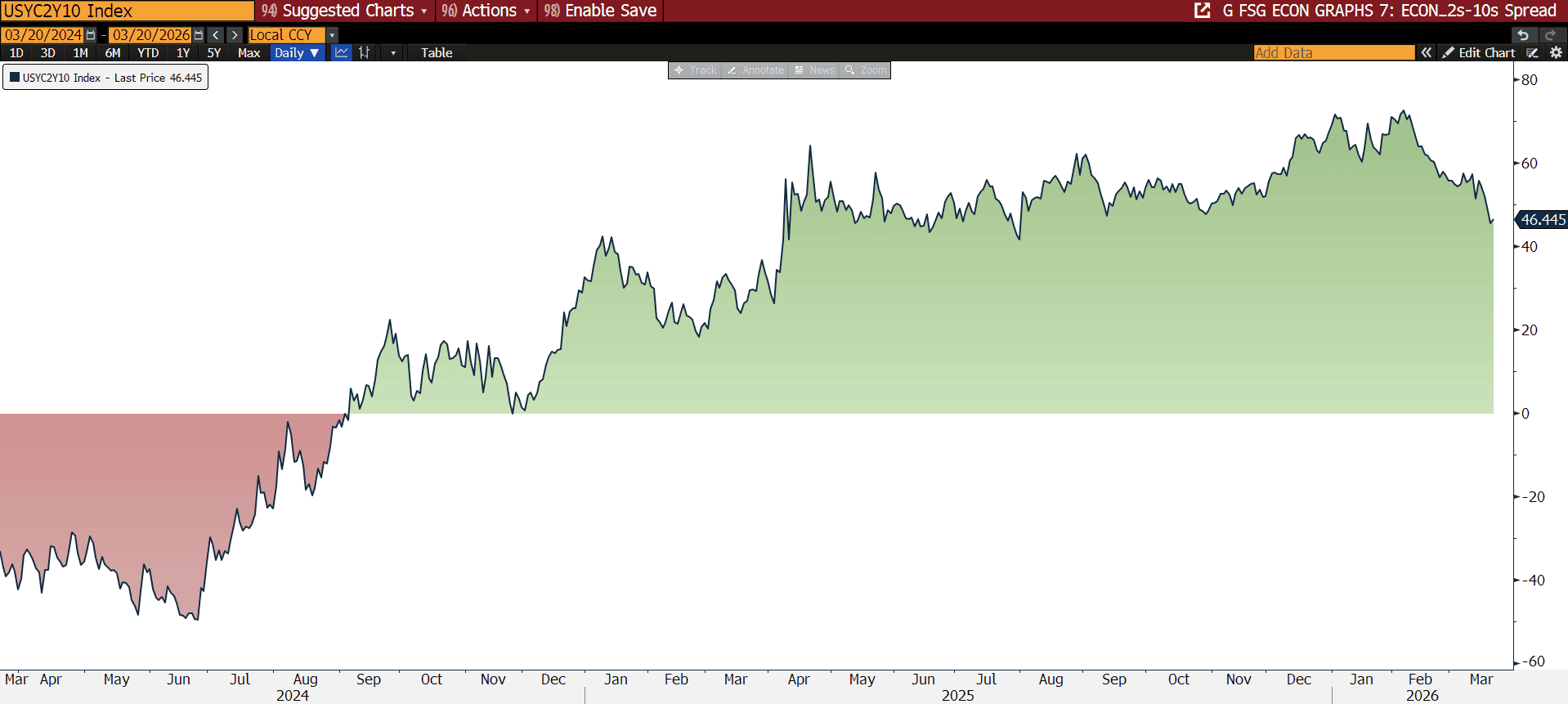

Market movement this week led to a flattening yield curve as the spread between the 2yr Treasury and the 10yr Treasury moved down by around -12bp. Market participants had been pricing in 1-2 rate cuts from the Fed throughout this year, but those expectations are now being priced out of the market following the FOMC meeting on Wednesday. Ironically, the Fed maintained its own expectation of one rate cut this year, but the market has gone from overpricing the Fed by one cut to underpricing the Fed by one cut. This divergence between the market and the Fed is being driven by a change in the inflation picture since the conflict in the Middle East began.

The Fed's dual mandate requires it to maintain maximum employment and long-term price stability. Prior to the engagement with Iran, the employment situation was seen as the greatest risk to that mandate, as the economy had just shed -92k jobs in February. Now that crude oil prices have increased roughly 40% since the end of February, the market has started to shift more attention to the inflation side of the mandate. Unfortunately for the Fed, the tool they use to manage both sides is the same. They raise rates when inflation gets too hot and they cut rates when the employment situation deteriorates. As both sides of the mandate currently appear to be slipping in the wrong direction, the Fed is forced into "wait and see" mode, and that's exactly what we saw as the Fed left rates unchanged in its meeting Wednesday.

Chairman Powell stated in his press conference, "The thing that's really important that we see this year is progress on inflation through a reduction in goods inflation as time effects of tariffs go through the system – go through the economy. That's the main thing we're looking for… the forecast is that we'll make progress on inflation… it should come, as we start to see in the middle of the year progress on tariffs… the rate forecast is conditional on the performance of the economy". Breaking that comment down, the Fed still expects to see progress on inflation this year. The expectation is that tariffs won't be a long-term driver of inflation and oil prices should eventually stabilize as the conflict winds down. In that scenario, you can see why the Fed is still expecting a lone rate cut this year, but clearly that forecast will be dependent on the data that we receive over the coming months.

Next week's economic calendar looks fairly light. We'll get a look at the ADP's weekly employment change, Import Prices, PMI, and the University of Michigan's consumer sentiment report.

Source: Bloomberg

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dillon Wiedemann

Senior Vice President of FSG

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.