Today’s Baker Market Update comes to you a full day earlier than usual due to observance of Juneteenth tomorrow. This week wasn’t necessarily full of key economic releases; however, all eyes were on the Fed as the Federal Open Market Committee met for its two-day June meeting, which was the first meeting of the newly appointed Fed Chairman, Kevin Warsh. Let’s dive in!

The FOMC’s statement was one of the briefest statements I can remember. To no surprise, the committee decided to keep rates unchanged. Since the statement was so brief, I included the last part of it below. “Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.” On inflation, the statement added: “Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.”

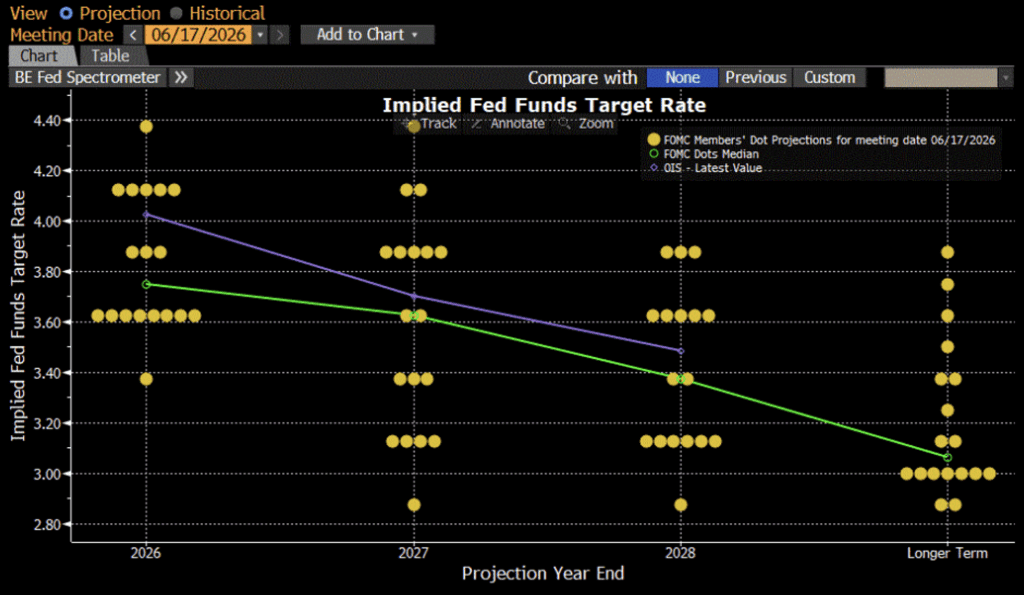

Although the statement didn’t provide much insight into the committee’s mindset, we must turn to the updated Fed Dot Plot and Chairman Warsh’s first press conference. The committee’s updated Dot Plot turned more hawkish as the median estimate for the Fed Funds rate at the end of this year rose to 3.8%, up from 3.4% in March. This implies that the median committee member now sees at least one rate hike this year. Another key Dot Plot note is that Chairman Warsh was the missing dot. He confirmed that he refrained from submitting any projection as he is critical of the Summary of Economic Projections as it is currently structured. During his first press conference, Warsh said, “we’ve dropped forward guidance” and they are establishing various task forces covering five areas central to the broad conduct of monetary policy. He stated that his expectation was that the task forces would begin work in the next couple of weeks.

Bond markets sold off and stocks were down sharply after Chairman Warsh’s press conference as investors grew uncertain over the path of monetary policy after a number of Fed officials see at least one rate hike this year.

There were some other economic releases this week, including advance retail and food-services sales which rose 0.9% month-over-month, beating the 0.5% consensus and were up 6.9% from a year earlier. This report points to solid consumer demand. Housing was the week's weak spot. Housing starts fell 15.4% from April to a seasonally adjusted annual rate of 1,177,000, 8.7% below May 2025. Single-family starts slipped 1.9% to 882,000. Building permits fell 0.7% to 1,413,000, while single-family permits rose 0.6% to 886,000. Completions dropped 8.1% to 1,313,000.

Lastly, this morning, initial claims fell 4,000 to 226,000, slightly above the 225,000 estimate. The four-week moving average rose to 223,250. Continuing claims moved up 24,000 to 1.810 million.

A look at this morning’s markets shows that stocks have rebounded slightly as Treasuries are rallying after yesterday’s afternoon sell-off. Looking ahead to next week’s economic releases, we’ll see a handful of releases on Thursday including May’s PCE inflation release.

Have a great weekend!

Federal Open Market Committee – June Dot Plot

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dale Sheller

Managing Director

Director of Financial Strategies Group

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.