With the most divided Fed in over 30 years and optionality risk hiding in plain sight, portfolio managers who will win in this environment are the ones who understand exactly what they own — and why they own it.

Simply getting through the past five years of balance sheet management deserves some recognition. Between a global pandemic, a 525-basis-point rate tightening cycle, and a record liquidity squeeze, there has been no shortage of challenges. But as we look at the current environment, it is becoming increasingly clear that the next phase may be just as demanding — and the institutions that are acting with intention right now will be far better positioned than those still waiting for clarity.

At its April 2026 meeting, the FOMC held rates at 3.50–3.75% for the third consecutive time — but four members dissented, a level of disagreement last seen in 1992. Three regional Fed presidents pushed back against the committee’s easing-bias language, arguing that inflation remains too broad-based to justify any shift in stance. A fourth member has dissented in favor of a cut at every single meeting since joining in September 2025. Meanwhile, the majority is holding firm: inflation is still elevated due to the Middle East energy shock, the labor market is stable, and the path forward is anything but clear. As Powell put it: “You’ve got one tool, it can’t do two things at once.”

The incoming Fed Chair Kevin Warsh will inherit not just a complex macro backdrop, but a genuinely fragmented committee. For bank portfolio managers, this means the rate uncertainty that has defined the past several years isn’t going away. And that brings us to what I believe is the most underappreciated risk sitting in many portfolios today: optionality.

The Risk Nobody Is Watching

Most ALCO committees spend the bulk of their risk discussion on duration. And that makes sense — duration is measurable, modellable, and fairly intuitive. A five-year duration instrument loses roughly 5% in market value for every 100 basis points of rate increase. It’s a compensated risk. You choose to carry it, you get paid for it, and you can plan around it.

Optionality risk is a completely different animal. It is non-linear, path-dependent, and — critically — it is always working against you. The embedded option in a callable bond or an MBS security is held by the counterparty: the issuer or the borrower. They will exercise it when it benefits them, which by definition means it hurts you. When rates fall, they call or prepay and you’re forced to reinvest at lower rates. When rates rise, they extend and you’re locked into below-market coupons. It is asymmetric risk in the worst possible direction, and it hides inside instruments that most banks have owned for years without ever fully measuring the cost.

There are three distinct ways optionality shows up as a problem. Extension risk kicks in when rates rise: MBS average lives stretch dramatically, callable bonds go out of the money and simply stay on your books, and liquidity that you need gets trapped at below-market yields. Contraction risk is the mirror: when rates fall, borrowers refinance and issuers call, flooding you with cash at the exact moment yields are at their lowest. Volatility risk is perhaps the most overlooked. Even without rates moving directionally, elevated rate volatility causes the market to demand higher yield on optionality-heavy securities, which pushes prices down even on portfolios that would look fine on a standard parallel-shift stress test.

That last point is worth sitting with for a moment. A portfolio can pass every rate shock scenario in your standard ALM model and still be silently impaired because those models don’t reprice options across scenarios. If your analytical approach is limited to nominal yield and modified duration, you are not seeing the full picture of what you own.

Oversteering and the Overcorrection Loop

One of the behavioral patterns I see most often — and that I think is worth naming directly — is the tendency toward overcorrection. Portfolio managers who have been burned by optionality sometimes respond by making very large moves at exactly the wrong time. This creates an overcorrection loop: large adjustment, large swing in the opposite direction, another large adjustment. The portfolio never settles into genuine alignment with the balance sheet. It chases the last crisis instead of preparing for the next one.

Think of it like steering a large boat. There is a significant lag between your input and the vessel’s response. Inexperienced drivers overcorrect every time, swinging back and forth across the intended line. Experienced ones make small, early adjustments and wait patiently for the response before touching the wheel again. The same principle applies here. Small, proactive moves guided by a clear understanding of your optionality exposure are far more effective than reactive lurches driven by pain.

The good news is that we now have the tools to make those early, informed adjustments. Effective duration, convexity, OAS, and average life analysis across multiple prepayment scenarios — used consistently, before purchases rather than after — give us the information we need to stop relying on nominal yield as our primary decision-making metric.

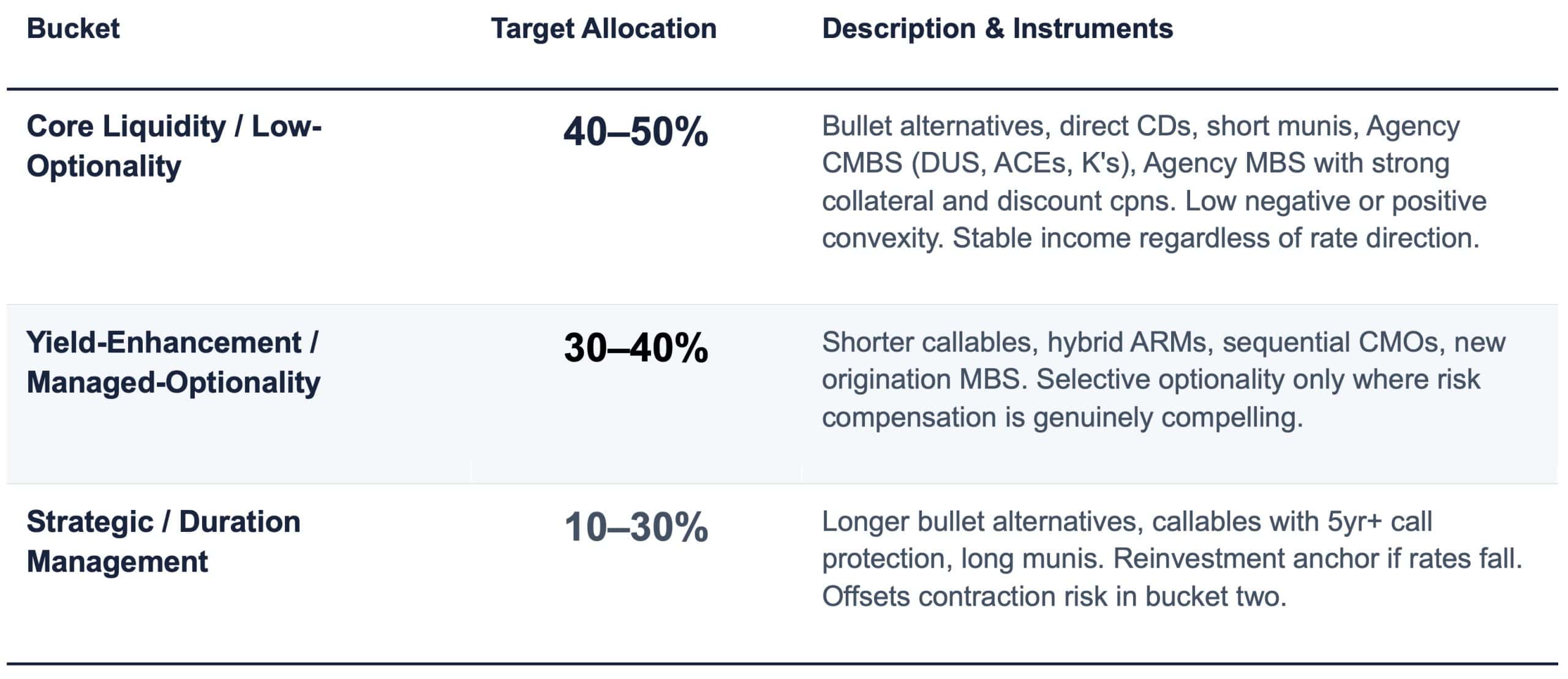

A Framework for What to Own

Rather than prescribing a single strategy, I’d encourage management teams to think about the portfolio in three distinct buckets, each with a clear purpose:

TARGETED PORTFOLIO ALLOCATION FRAMEWORK

Recommended allocation ranges by strategy bucket

The Playbook for the Rest of 2026

So where does all of this leave us practically? Here are the actions we believe deserve the most attention between now and year-end.

- Lock in coupons while you can.

Bullet alternatives still offer strong yields today. The asymmetric risk clearly favors acting: if rates fall, locking in today’s yields generates significant upside. If rates rise modestly, the loss is manageable. Waiting for more certainty is itself a risk position. - Limit adding new optionality at current spread levels.

Volatility is elevated, and OAS spreads on callables and current-coupon MBS are tight. You are not being adequately compensated for the option risk you would be taking on. Bullet alternatives and lower-coupon, seasoned MBS offer more reliable income on a risk-adjusted basis right now. - Stress before you buy.

Run prepayment and call scenarios on every optionality-bearing security before purchase. If the risk-adjusted yield effectively disappears under a rate shock, you are paying a hidden fee to absorb option risk that you are not being compensated for.

Perhaps the most important mindset shift is recognizing that the investment portfolio is no longer – if it ever was – a passive resting stop for excess cash. In today’s environment, it is a core balance-sheet tool. Yesterday’s paradigm was yield first, reactive and siloed from ALM decisions. Today’s approach demands that every investment decision begin with balance sheet’s current position and needs. What duration, cashflow, or liquidity gap needs to be closed? What structure and convexity best addresses that gap without creating new optionality exposure?

None of this requires predicting where rates are going. Frankly, I don’t know where rates are going, and I would be skeptical of anyone who claims they do with confidence right now. That is not the point. The point is that a proactive, structurally sound portfolio — built around a clear understanding of what each security does to your balance sheet across different rate scenarios — will outperform a reactive, yield-chasing book in virtually any environment.

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Andrew Okolski

Managing Director

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.