Happy Friday everyone, and welcome to this week's Baker Market Update! Per usual, before we get started, I would like to mention that our beloved Oklahoma City Thunder lead the Los Angeles Lakers 2–0 after last night's 125–107 win. The series will resume in Los Angeles tomorrow evening.

This week had no shortage of labor market data to digest, and this morning's Employment Situation report from the BLS was the main event. April nonfarm payrolls came in at 115k, which was softer than last month, but nearly double what forecasters were pricing in at 65k. The unemployment rate stayed put at 4.3%, and hourly wages for private nonfarm workers nudged up 0.2% to $37.41, now running 3.6% above prior year's levels. Health care, transportation and warehousing, and retail trade did most of the heavy lifting on the jobs side, adding 38k, 30k, and 22k respectively. On the federal side, government payrolls shed another 9k in April and are now down 348k from their October 2024 peak. Wednesday's release of the ADP National Employment Report added another data point to this week's labor market picture. Private sector employment grew by 109k in April, coming in below the 120k analyst estimate but representing a meaningful pickup from the 62k increase recorded in March, pointing to a modest improvement in private hiring activity on a month-over-month basis.

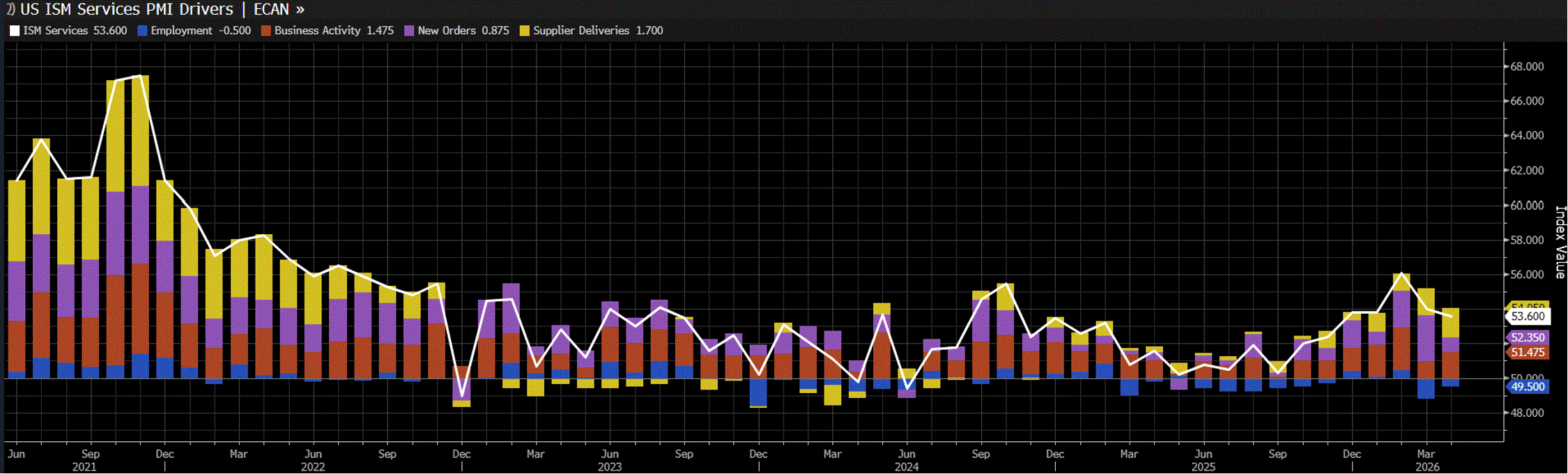

The Institute for Supply Management's Services PMI hit the tape on Tuesday, giving us the latest read on U.S. service sector conditions. April's print of 53.6 came in just a tick below both the 53.7 estimate and the prior reading of 54.0, continuing a slow drift lower from the stronger values we saw at the start of the year. As a diffusion index, anything above 50 tells you the sector is still expanding on net, and at 53.6 that remains the case, though the mild deceleration we have seen in recent months does suggest the pace of growth is gradually tapering from its earlier highs. Tuesday also brought the S&P Global US Services PMI, which echoed much of the same narrative, reinforcing the picture of a services sector that is still growing but losing a bit of steam.

Next week we will get key data points regarding inflation at both the consumer and producer level via the Consumer Price Index and Producer Price Index, as well as some manufacturing data. Have a great weekend everyone!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Carson Francis, CFA

Financial Analyst

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.