Happy Friday everyone! We are getting close to the end of the school year and the beginning of summer. The sun is out and temperatures are rising, but they are not the only thing that came in hot this week. Back-to-back hotter than expected prints on CPI and PPI rattled bond markets and reignited fears that the Fed's next move could be a hike rather than a cut. Bond yields are up this morning as the fog of uncertainty surrounding the conflict in the Strait of Hormuz continues to roll on. The stock market did see some mid-week jumps as optimism surrounding President Trump's summit with Chinese President Xi Jinping sent the S&P 500 above 7,500 and the Dow Jones back above 50,000 for the first time since February, but have slightly backed off those highs this morning.

Tuesday brought April's Consumer Price Index, and it was not the reading markets, or the Fed, were hoping for. Headline CPI rose 0.6% for the month and 3.8% year over year, which was the highest annual reading since May 2023 and above the consensus estimate of 3.7%. Energy prices jumped 3.8% and accounted for over 40% of the monthly gain, with gasoline up 28.4% annually. Energy prices are expected to remain elevated as long as the conflict in the Middle East continue and US Oil Prices (West Texas Intermediate) stay above $100 a barrel. While energy was a large contributor to inflation, it was not the only factor in the hot CPI print. Core CPI, which strips volatile food and energy prices, came in at 2.8% year over year and slightly edged higher than estimates of 2.7%. To add insult to injury, real average hourly wages slipped 0.5% for the month, meaning workers are once again losing ground to prices and real wage growth is feeling the pressure.

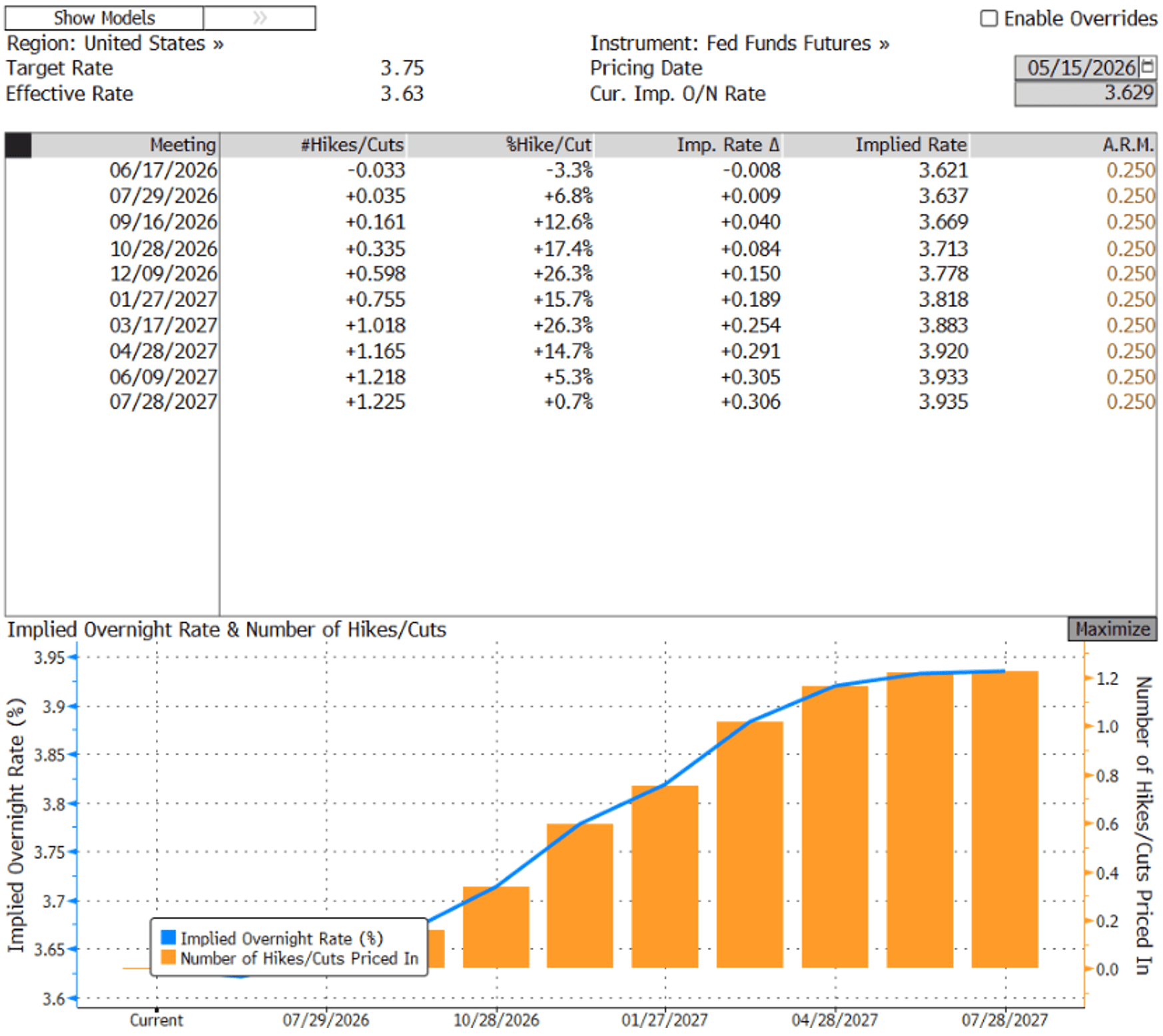

If Tuesday's CPI felt like a punch to the gut, Wednesday's Producer Price Index felt like the People’s Elbow from the top rope. April PPI surged 1.4% month over month, close to triple the 0.5% estimate and the largest monthly gain since March 2022. On an annual basis, final demand PPI hit 6.0%, the highest since December 2022. Core PPI rose 1.0% against an estimate of just 0.4%. The services component jumped 1.2% for the month, with two-thirds of that move tied to a surge in trade services. PPI is often called the "pig in the python," and what is moving through the wholesale pipeline today tends to show up in consumer prices tomorrow. Following both prints, the market-implied probability of a Fed rate hike by year-end climbed to roughly 60% according to Bloomberg’s World Interest Rate Probability model and a full chance of a rate hike priced in by March of 2027.

Thursday's retail sales report offered a mixed picture. Headline sales rose 0.5% in April, in line with estimates and marking the third consecutive monthly gain. However, gasoline station receipts climbed 2.8% and are up over 20% annually, which accounted for much of the heavy lifting. Excluding gas, discretionary categories struggled. Furniture stores, clothing retailers, department stores, and auto dealers all posted monthly declines, suggesting consumers are increasingly prioritizing necessities over wants. The term 'resilient consumer' has been tossed around for the last few years, but as inflation starts to poke its head back out, cracks have started to emerge.

Today also marks a significant transition at the Fed, as Chairman Jerome Powell's term officially ends and Kevin Warsh steps in as the new Chair. Two straight inflation shocks will likely limit any room to ease early in his tenure. Next week brings pending home sales on Tuesday, FOMC minutes on Wednesday, and wraps the week up with the University of Michigan’s Consumer Sentiment report on Friday. Have a great weekend everyone!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Luke Mikles

Senior Vice President of FSG

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.