The 10yr Treasury started the week trading around 4.45% and sits at 4.53% as of the time of this writing, as green shoots in a recently struggling labor market have begun to get priced in. The week's calendar was decidedly jobs heavy. Tuesday's JOLTS report showed job openings jumping to 7.618M (est = 6.866M), with the openings rate climbing to 4.6% from 4.2% the prior month. Layoffs also fell, to 1.692M (est = 1.842M), as did quits, to 2.977M (est = 3.138M), a mix that points to firmer labor demand and less slack than the market had been positioned for.

That theme came to a head Friday with a payrolls report that landed well above expectations. Employers added 172k nonfarm payrolls in May (est = 88k), and the prior two months were revised up by a combined 93k. That lifts the three-month average to 188k, the strongest run since March 2024. Hiring was concentrated in leisure & hospitality (+70k), government (+52k), and health care (+47k), while financial activities (-22k), private education (-7k), and trade (-5k) posted the largest pullbacks. The separate household survey added 149k jobs, its first gain in five months, which kept the unemployment rate anchored at 4.3% for a fourth straight month even as labor force participation held at 61.8%. Average hourly earnings rose 0.3% on the month and 3.4% year-over-year. The strength of this report suggests labor demand could be holding up better than initially feared, while wage growth remains right at its 30yr average of 3.4%.

The rest of the week's data was firmer than expected but didn't change the market’s picture. Both ISM surveys beat, with manufacturing at 54.0 (est = 53.0) and services at 54.5 (est = 53.8), and prices-paid stayed elevated at 82.1 and 71.3, a sign input cost pressure remains somewhat elevated. Capital Goods Orders Nondefense Ex-Air, which is a proxy for business investment, slipped by -1.0% for the month.

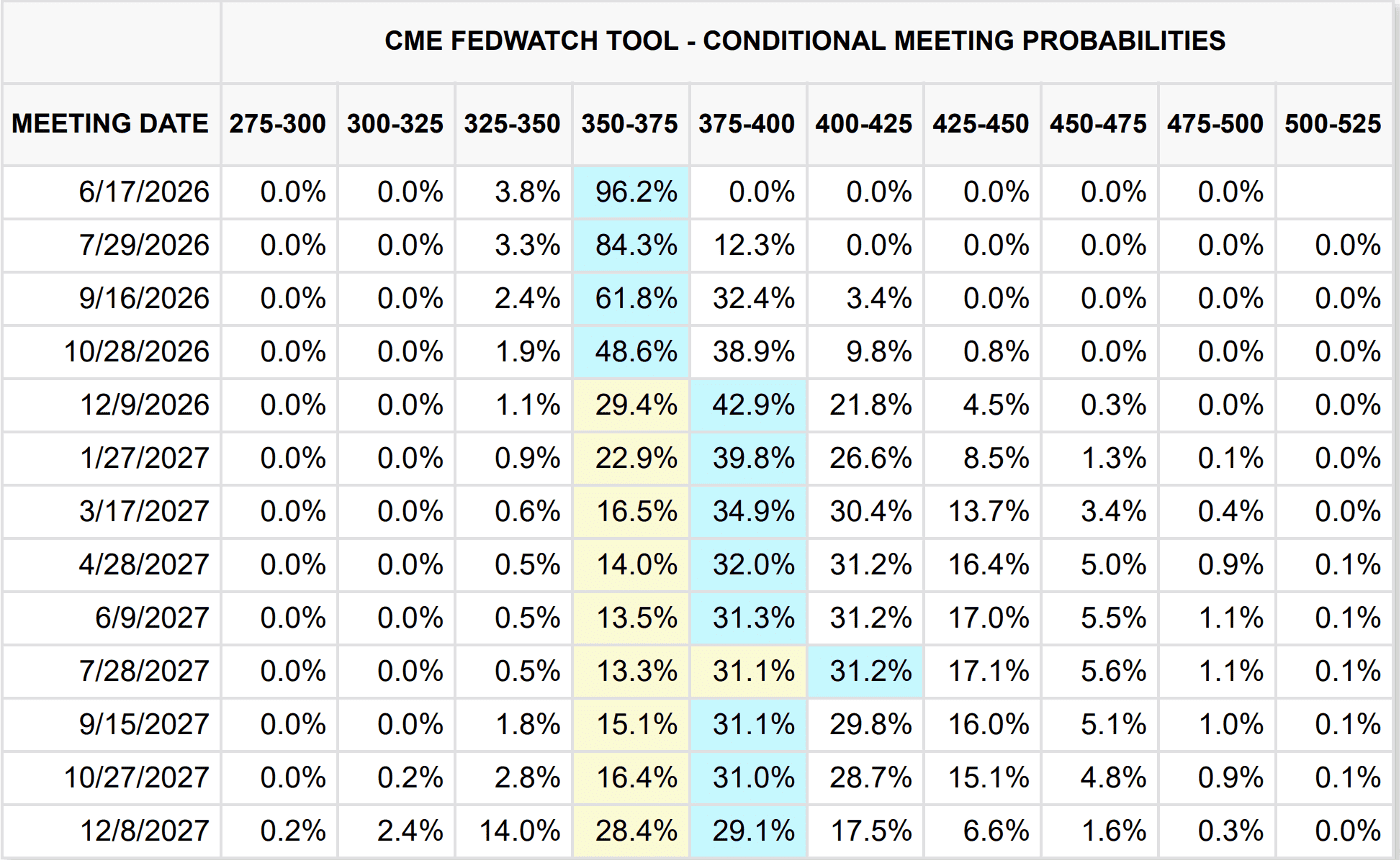

Taken together, the week's data all but removes rate cuts from the table this year barring a sharp turn in the data. The timing is notable, as the June FOMC meeting lands just 10 days out and will be Kevin Warsh's first as Fed Chairman. It is likely that the Committee will drop its easing bias in the June statement, with the updated dot plot likely showing few members favoring cuts this year and possibly several leaning toward hikes.

Friday's Non-Farm Payrolls print drove the bulk of the week's market repricing. The 2yr surged 9bp to 4.13% and the 10yr added 6bp to reach the 4.53% noted above. Fed funds futures are now pricing a hike by December.

Looking ahead to next week, we’ll get a look at the NY Fed’s 1yr Inflation expectations, CPI, PPI, and University of Michigan’s consumer sentiment index. The market will likely be paying a lot of attention to the final CPI report before Chairman Warsh’s first meeting. Surveys anticipate that the headline CPI number will come in at 4.2% for the month.

Hope everyone has a great weekend!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dillon Wiedemann

Senior Vice President of FSG

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.