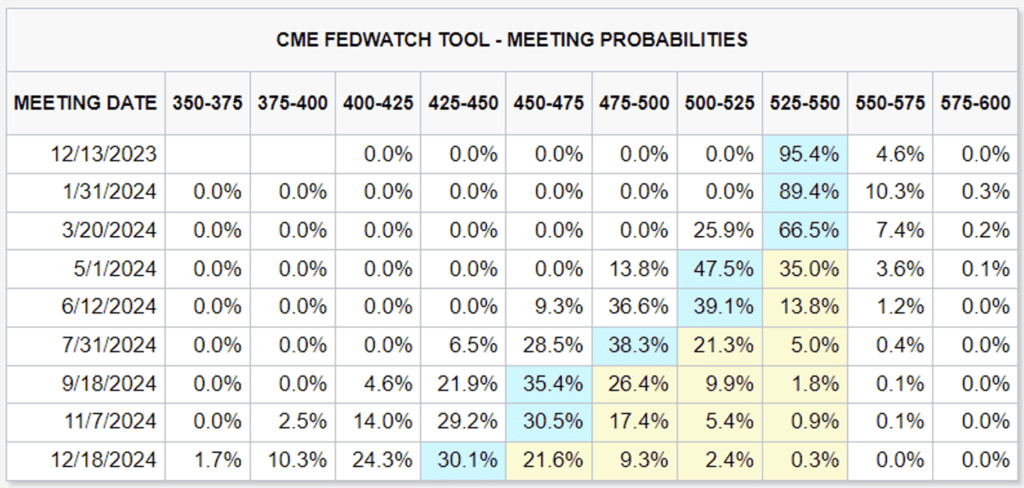

“Put a fork in it – they are done”, says Wells Fargo Co. Chief Economist, Jay Bryson, after this morning’s jobs numbers came in much lower than expected. Payrolls for the month of October increased by 150,000 compared to 180,000 estimated, this is a sharp decline from the revised gain of 297,000 the prior month. Health care led the way with 58,000 new jobs and manufacturing posted a decline, mostly attributed to the auto worker strikes. The unemployment rate rose to 3.9% (est. 3.8%), the highest level since January 2022, amid a sharp decline in household employment. This will be welcome news for Fed officials that elected to maintain the Fed Funds Rate at 15yr highs earlier this week and are “proceeding carefully” with regards to future rate hikes. Yields on the 10yr Treasury are down -13bps this morning, based on market sentiment that the jobs report could be enough to give Fed officials the data they need to end their hiking campaign against inflation. While this is good news, bond investors should remain diligent as the Fed has maintained they are going to be data-dependent throughout this hiking process and any evidence of an increase in inflation could be enough for the Fed to continue its hawkish policy. Still yet, slower payroll growth is a good step in the right direction for the Fed and lends credence to David Rosenburg’s presentation at our OKC Seminar in October about the state of the consumer (Linked Here). It’s an excellent presentation and well worth the listen if you haven’t already heard it.

Outside of the Fed’s decision to maintain current rates, we also got a look at the ADP Employment Change report. This report reflected an increase in private payrolls of 113k vs 150k expected. Tuesday’s Conference Board Consumer Confidence Report showed deteriorating consumer confidence levels for the month of October. This monthly report details consumer attitudes, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates.

Next week’s economic calendar will be light and should give markets time to adjust. Initial Jobless Claims and Continuing Claims will be closely watched next week as traders look to validate October’s unemployment numbers. We’ll also get a look at the US Census Bureau’s Trade Balance Report and the University of Michigan’s Consumer Sentiment preliminary report.

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dillon Wiedemann

Senior Vice President of FSG

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.