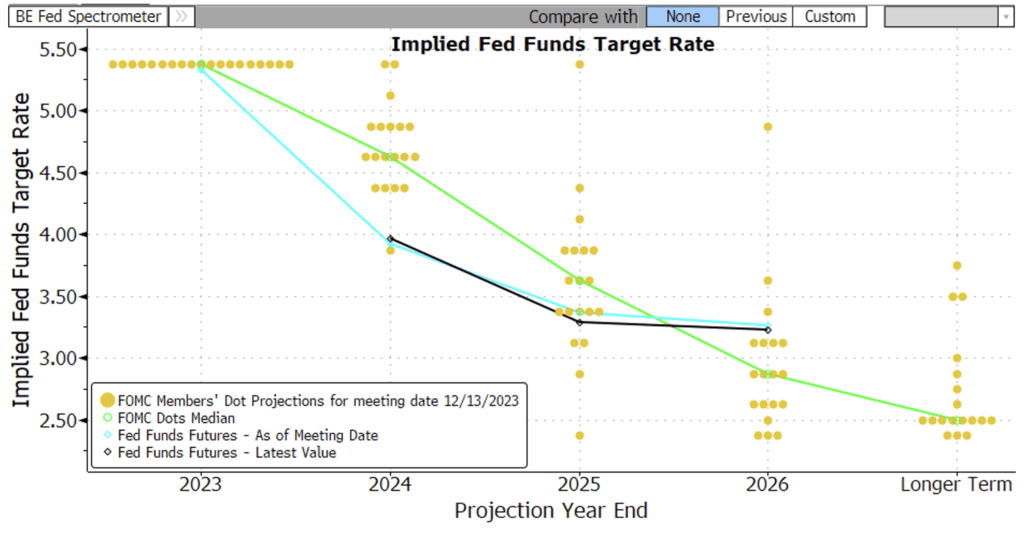

What a difference a week makes. Last week the 2yr yield plunged 24bp as markets priced in one additional rate cut this year bringing total expected cuts to 150-175bp. That was driven by relatively tame inflation reports and flight to quality buyers worried that US airstrikes in Yemen would spill over into a broader Mideast war. Fast forward to this week and the 2yr yield jumps 25bp as markets price out the rate cut they priced in last week! Why? This week the tensions in the Mideast settled down and we got better than expected economic reports on Retail Sales, Industrial Production, Housing Starts, Building Permits and Initial Jobless Claims. While all the data wasn’t exceptionally strong, there were enough reports that beat expectations in different sectors of the economy to convince traders that the Fed will be less aggressive in cutting rates this year. Fed funds futures are now pricing just a 50% chance the Fed cuts in March and a total of 125-150bp of rate cuts for all of 2024. But why is the market pricing in twice as many rate cuts as the Fed’s latest Dot Plot says they expect to cut (75bp)?

I think the main reason relates to the economic data the Fed focuses on versus what traders and investors watch. The Fed is mandated to maximize employment and achieve price stability so they must focus on the actual incoming data on unemployment and inflation (PCE, CPI, PPI, etc). Those data points are known as lagging economic indicators since they only tend to turn after the economy has turned down. Traders and investors are trying to anticipate whether the economy will turn down before it actually does so they tend to focus on leading economic indicators like building permits and manufacturing new orders. Unemployment remains low and the latest inflation reports are still above the Fed’s 2% target so the Fed says only 75bp of cuts and probably starting in the second half of the year. But leading economic indicators have fallen for 20 consecutive months (a stretch never before seen without a recession) so traders are forecasting the economy will decline and the Fed will be forced to cut soon and twice as much as they say they will. So either the data needs to weaken like the market is anticipating or yields have to backup to match the path of rates laid out in the Dot Plot. And that is exactly what happened this week as traders priced out one 25bp rate hike in 2024 and that caused the 2yr yield to rise 25bp.

Next week we’ll could see some volatility with reports on Leading Economic Indicators, Q4 GDP, Durable Goods, New Home Sales, Personal Income & Spending and the Fed’s preferred measure of inflation, the PCE Deflator.

FOMC December 2023 Dot Plot

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Ryan W. Hayhurst

Managing Partner, President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.