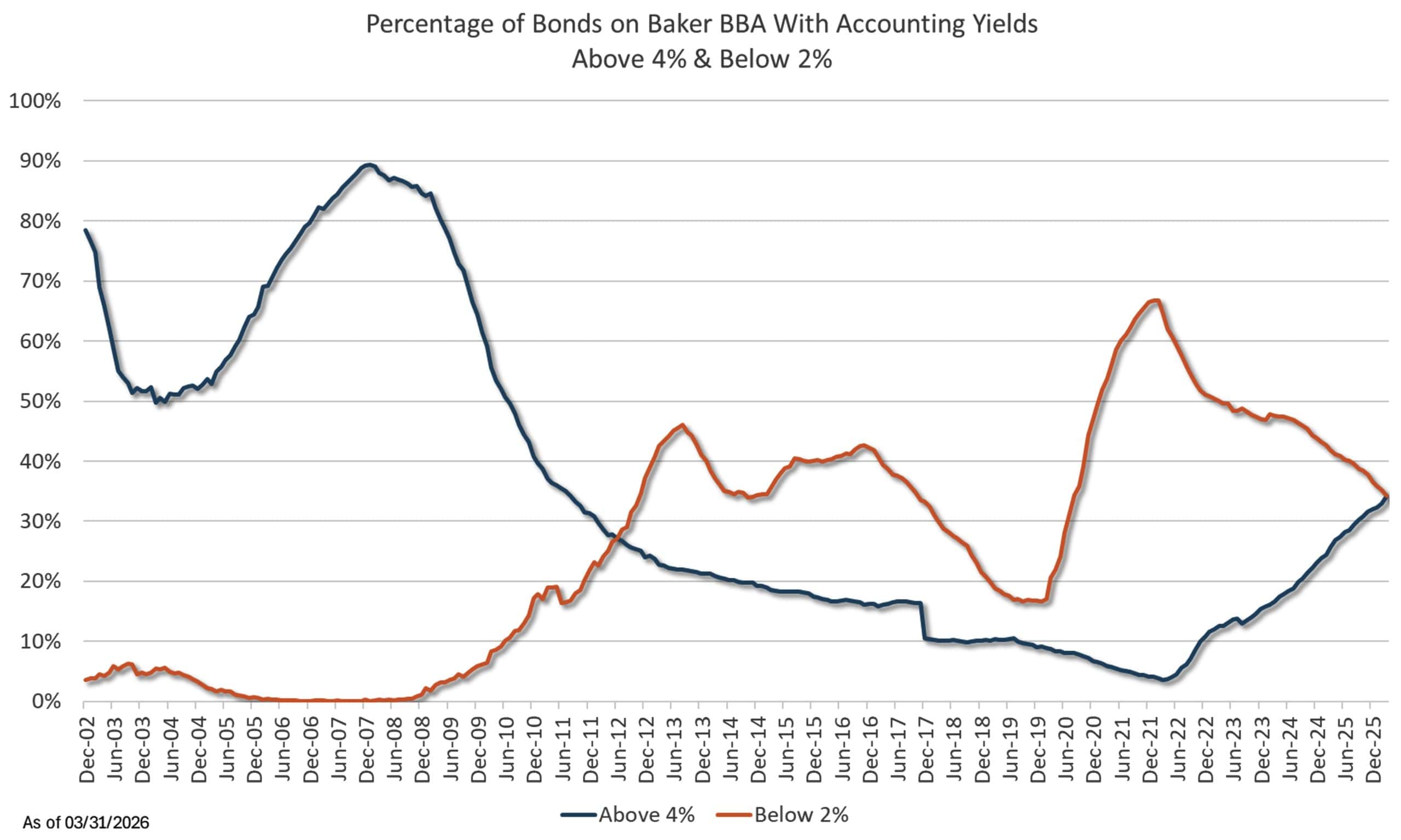

For more than a decade, community bank bond portfolios languished under the weight of the Fed’s zero interest rate policy, or ZIRP. Portfolios filled with higher yielding bonds that matured or got called away, saw their yield slowly erode as the average bank portfolio yield fell from more than 5% in 2007 to less than 2% in 2021. In fact, bank holdings of low-yielding bonds (I’ll define that as less than 2%) have exceeded their holdings of high- yielding bonds (greater than 4%) for the last 13 years. But the Fed’s aggressive tightening cycle of 2022-23 and the subsequent surge in bond yields have helped banks turn the page on the era of low yielding bonds.

For the first time since 2012, the percentage of bonds yielding 4% or more has surpassed the percentage yielding less than 2% (see chart). It's a crossover that most bankers didn't dare imagine just a few years ago. And it represents both a milestone worth celebrating and a call-to-action portfolio managers can't afford to ignore.

How We Got Here

To understand where bond portfolios stand today, it helps to rewind to the era before the financial crisis. In 2007, nearly 90% of the bonds held by community banks carried yields above 4%. Rates were high, yield was plentiful and the idea that the Federal Reserve could actually cut rates to zero was considered crazy.

Then came 2008. The Federal Reserve slashed rates to zero in response to the financial crisis and kept them there for years. As higher-yielding bonds matured, got called, or prepaid ahead of schedule, banks reinvested the proceeds into a market offering historically low yields. By 2012, the percentage of sub-2% bonds owned by banks had surpassed the share of bonds yielding more than 4% — and it stayed that way for more than a decade.

The pain was compounded further when rates finally did rise sharply in 2022-23. Banks sitting on portfolios stuffed with 1-2% bonds watched their unrealized losses balloon, constraining capital, complicating balance sheets, and limiting strategic flexibility. It was, for many institutions, the worst of both worlds.

The Crossover Moment

But along with unrealized losses came significantly higher reinvestment opportunities and the same forces that once worked against banks are now working in their favor. Low-yielding bonds have continued to mature while the 2021-23 surge in bond yields opened a window — one that many proactive banks took advantage of aggressively — to purchase bonds at yields that hadn't been available since before the financial crisis. Data from more than 600 community banks on The Baker Group’s Baker Bond Accounting (BBA) system now shows that high-yielding bonds have finally reclaimed the lead, exceeding holdings of low-yielding bonds for the first time in over 13 years.

The banks that moved decisively during that window are the ones seeing the strongest improvement in their yields today. The message is clear: activity matters. The more bonds a bank has purchased over the last three years, the better their portfolio composition looks right now.

The Corner Isn't the Finish Line

Turning the corner is meaningful — but it's not the moment to ease off. The Federal Reserve has already cut rates by 175bp and ultimately wants to lower rates to around 3% once the threat of higher inflation subsides. Any further rate cuts and subsequent slide in bond yields may give way to reinvestment opportunities that look more like the post-2008 era than the post-2022 era. We've seen this movie before, and banks that hesitated last time spent years wishing they hadn't.

The good news is that most institutions still have meaningful options today. The question is whether they'll act on them and act quickly enough to matter.

Keep the Momentum Going

If your portfolio still carries a heavy concentration of sub-2% bonds, or if you simply want to press the advantage while the rate environment still allows it, there are some concrete steps you can take today.

Deploy Cash — Many banks are still holding excess liquidity at the Federal Reserve or in overnight instruments. This may have seemed like the best option when the yield curve was inverted and cash yielded more than bonds, but that has changed. The yield curve is positively sloped once again and banks can earn 50-150bps more yield by deploying cash into the bond portfolio. Every dollar sitting in cash is a dollar that could be working harder in the investment portfolio for years to come. Extending even a portion of that liquidity into intermediate-term, higher-yielding securities locks in today's rates before the market moves away from you. It's the lowest friction move available and a natural place to start.

Consider Bond Restructurings (Swaps) — Selling low-yielding securities at a loss and immediately reinvesting into higher-yielding alternatives, often called a bond swap, is one of the most effective tools available for accelerating the improvement in your portfolio's yield profile. Yes, it means realizing a loss today. But if the math works, you recoup that loss through higher earnings in a relatively short period and emerge with a meaningfully better portfolio. With today's rate environment still offering yields well above historical averages, the spread between what you're selling and what you're buying can make the numbers very compelling.

Build a Systematic Reinvestment Discipline — Rather than waiting for the "perfect" moment to buy, consider a disciplined reinvestment program that consistently deploys cash flows from maturing bonds, calls, and prepayments into new purchases at current yields. Consistency compounds over time, and staying active keeps your portfolio moving in the right direction even when markets feel uncertain.

Update Your Investment Policy and ALCO Process — Perhaps the most durable thing you can do is embed this momentum into your institution's governance. Make sure your investment policy explicitly allows tax-loss swaps when the earn-back math is favorable and the new securities improve your overall risk metrics. Many policies are silent on this, which creates unnecessary hesitation at exactly the wrong moment. Portfolio managers can also add a quarterly "portfolio refresh" item to every ALCO agenda: review the investment portfolio and ensure performance is meeting or exceeding your expectations. If it isn’t, set a realistic target for the next twelve months and take action. What gets measured gets managed, and making this process a standing agenda item ensures the progress you've made doesn't quietly erode between cycles.

The Bottom Line

The improvement you're seeing in community bank yields isn't just a chart, it's a roadmap. It shows that the banks willing to act during a challenging rate environment are building portfolios that will serve them well for years. Turning the corner is a real achievement. Staying on course after you've turned the corner is the harder discipline, and the more important one. The window is still open. Make the most of it while the opportunity remains.

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Ryan W. Hayhurst

Managing Partner, President

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.