In early 2020, municipal credit concerns were abundant and tax revenue plunged due to pandemic shutdowns. Since then, average state and local tax revenue has not only recovered from those declines but has grown significantly. Total state and local tax revenue reported by the US Census Bureau was up 13.9% in the first half of 2022 when compared to the first half of 2021, and by over 30% when compared to the first half of 2019. Federal stimulus funds, coupled with prudent expense management, also helped to improve municipal finances, all of which led to record budget surpluses and large increases in reserves in many cases. However, current high inflation and increasing interest rates could impact municipal finances in several ways.

First, the cost of supplies and labor is increasing rapidly, in some cases at an even higher rate than the overall inflation rate. Consequently, operating expenses and the cost of capital projects are climbing. Issuers that are highly reliant on skilled labor for operating activities, such as hospitals and other healthcare-related entities, are vulnerable to a tight labor market. Moody’s reports that personnel costs account for over 50% of expenses for the hospitals they rate. Some issuers have had to pay over eight times as much in 2022 as they did in 2019 for agency labor. Rural hospitals are particularly susceptible as they generally have a hard time with adequate staffing under normal circumstances.

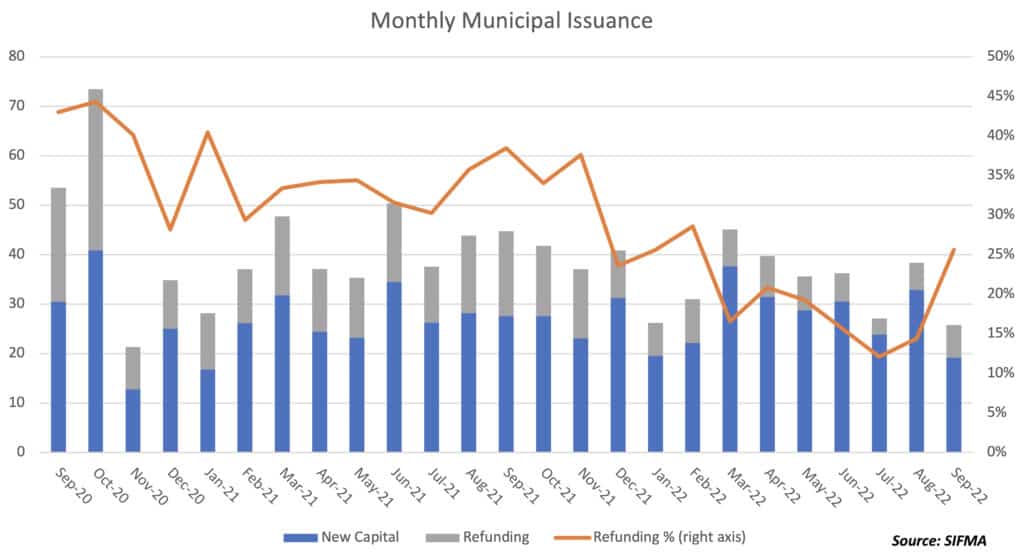

Second, not only are capital projects more expensive than what was estimated for current budgets, but borrowing rates have also been rising. This could result in delayed or canceled projects, or it may lead to higher debt levels and increased interest expense if municipalities choose to go ahead with planned projects. According to SIFMA, September issuance data shows that new money issuance dropped dramatically in September. As rates continue to rise, issuers will have to balance their capital needs with how much interest they can afford to pay.

Third, inflation and higher interest rates can affect pension liabilities and associated expenses. Pension liabilities are computed using assumptions for wage growth and expected inflation. If those assumptions increase or are too low, pension liabilities will increase. Some pension plans have cost of living adjustments based on inflation. Those plans will have an increase in current payouts in addition to an increase in the future liability. Further, pension assets will likely suffer from poor investment returns this year. The trend of movement toward riskier asset classes led to favorable outcomes in 2021, when many plans had record investment gains. However, the opposite may be true in this volatile environment where equities and bonds have both been declining in value. Moody’s and S&P both project that all the investment gains pension plans enjoyed last year will be, or already have been, reversed. Assets decreasing while liabilities are increasing means that unfunded liabilities will rise, and so will required contributions from employers. This may cause budget pressure for some municipalities.

On a more positive note, higher inflation and/or interest rates could increase the discount rate used to determine the present value of pension liabilities. A higher discount rate means a lower estimate of pension liabilities, all else equal. Also, inflation could lead to increases in revenue, particularly for those municipalities that rely heavily on income tax revenue or sales tax revenue derived from the sale of non-discretionary items. Discretionary spending is threatened by a potential recession as well as higher interest rates. Property tax revenue should increase as well since home prices have been increasing significantly. Higher home prices will lead to higher assessed valuations if home values do not depreciate back down to last year’s level or lower. Whether or not revenues rise by more than expenses will vary from issuer to issuer.

Many issuers have well-positioned reserves right now to help cope with increasing costs and a potential recession in the short-term. However, unfunded pension liabilities and growing leverage will continue to be a concern for some local governments. Many healthcare issuers, especially senior living facilities, and special development entities have experienced credit deterioration during the pandemic. They remain particularly vulnerable to further budgetary pressure and credit impairment due to current economic conditions. The Baker Group’s Credit Criterion Check monitoring system helps to identify issuers susceptible to weakening credit quality. Please contact your Baker representative for more information.

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Dana Sparkman, CFA

Executive Vice President/Municipal Analyst

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.